If an investor has the foresight to avoid investment bubbles, they have uncovered one of the most difficult elements to a successful long-term investment strategy. However, all too often, these bubbles are only identified with hindsight.

If an investor has the foresight to avoid investment bubbles, they have uncovered one of the most difficult elements to a successful long-term investment strategy. However, all too often, these bubbles are only identified with hindsight.

Emotions and market cycles – particularly those developed on fear and greed – mean that investment bubbles are likely to perpetually occur. In other words, it is euphoria which causes an investment bubble to form and fear that causes it to collapse. The Investing Times maintains thorough research on nine investment metrics that can potentially help identify the peaks and troughs in advance. Each have a tremendous track-record and should be added to every investors watch-list.

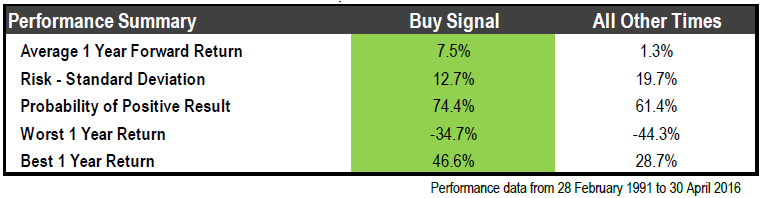

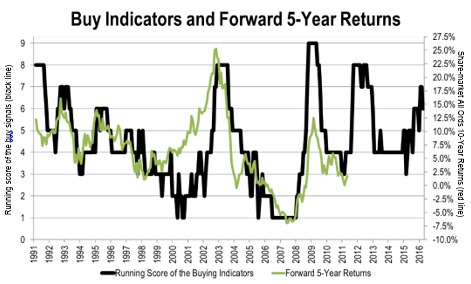

Below we identify these at a high level along with a performance extract from our Australian research database:

1. Shiller P/E Ratio – The Shiller P/E is a famous metric created by Robert Shiller who is a Professor at Yale University and Nobel Prize winner. His logic is that the traditional Price/Earnings gauge had two major flaws; firstly, that corporate earnings are too volatile, and secondly, that inflation needs to be considered to gauge long-term earnings. Hence he created a long-term gauge that assesses the past 10 years of real earnings (adjusted for inflation) and used this as a proxy for price. This creates a much more stable expectation of earnings upon which investors can make more reliable valuation estimates on price. As can be seen in the performance table, the Shiller metric has worked exceptionally well in Australia, which is backed by supportive global analysis.

2. Long-term Dividend Yield – The dividend yield can be considered one of the most under-rated components of an investment return. The dividend yield is calculated as the average dividend per share divided by the price. Therefore, a rising dividend yield implies that either a) companies are increasing dividends or b) that the price has fallen. The same applies in reverse. Given the negative correlation between dividend yields and the future price of the market, an opportunity exists to use dividends as a proxy for the long-term price of the market. While methods differ, our methodology takes the ‘regression average’ of the dividend yield over the past 15 years and compares this to the current dividend yield. Including a margin of safety, a buy indicator is apparent if the current dividend yield is 5% or more above the long-term average.

3. Market Capitalisation to GDP Ratio – Warren Buffett may be the world’s most famous investor and in recent decades he has unveiled his favourite metric to gauge the overall share-market. Buffett’s logic is that the size of all the listed companies in a given country should roughly track the overall size of the economy itself. The rationale is that business revenues are a subset of the economy and hence should match over the long-term. Therefore, the metric takes the market capitalisation of all companies and compares this to the GDP. Over the long-term, it has proven high-risk to invest when the market cap to GDP ratio exceeds 100% and low-risk to invest when it is low. We apply a margin of safety, so our methodology looks for times when the market cap is less than 90% of GDP for a buying signal.

4. The Zone System – Originally created by the founder of the Investing Times and the Australian Investors Association, Austin Donnelly, and then slightly modified thereafter, the Zone System is a long-term gauge of fair prices. The logic behind this system is that the market should average a very similar performance number over the very long-term, but this tends to fluctuate due to the economic cycle and sentiment surrounding fear and greed. Therefore, the Zone System allows an objective view by factoring in approximately two business cycles of historical analysis. Our application of the Zone System is to be willing long-term investors if the market is equal to or below its long-term average (i.e. Zones 3, 4 or 5). In reality, the further below the long-term moving average (i.e. Zone 5), the better the prospects for forward returns.

5. The Dividend Yield vs Bond Yield – The Yield Gap applies logic that investors are always making a decision between stocks and bonds (or growth assets and defensive assets). Therefore, it is common-sense to analyse the pricing of these together. There are various versions on the most appropriate application of this logic, but our methodology uses the market dividend yield compared to the Treasury bond yield over the long-term. By comparing the grossed up dividend yield of the overall market to the 10-year bond yield, we can clearly see which way investors might move their funds. For example, if bond yields are very high relative to stocks, a rational investor will move his/her money from stocks to bonds and vice versa. Our methodology uses the long-term moving average of these numbers and the grossed up dividend yield of at least 20% higher is desirable.

6. The 45-64 year old Demographic – The mature age working population is defined as the civilian population between the ages of 45 to 64. This is deemed to be the most important segment of the population for share-holders as these individuals are the most likely to be net buyers of shares. The logic behind this is that 45-64yo individuals are generally gearing up towards retirement and a combination of greater incomes with lower family commitments in general. The importance of tracking demographic trends is imperative as various reputable studies have shown a declining working population creates high risks of deflation and a 40% reduction in future GDP.

7. The Shape of the Yield Curve – A “recession factor” draws on a body of evidence, demonstrating the power of the yield curve in predetermining recessionary conditions. More specifically, an inverse yield curve is said to be one of the most reliable predictor of recessions among all financial data. Our application of tracking the yield curve is a simple calculation taking the 10-year government bond yield minus the 5-year government bond yield. The idea is to simply avoid the share-market during times when it is negative. It should be noted that a positive yield curve is considered normal as it factors in inflationary expectations and liquidity risks.

8. The Coppock Indicator – The Coppock Indicator is famous among technical traders but is arguably under-utilised by long-term value investors. E.S.C Coppock was a well-known economist in the 1960’s that utilised knowledge of behavioural patterns, especially around bereavement. Specifically, he found that the average human mourns for a period of approximately 11 to 14 months on average before finding stability. Coppock’s logic was that investors experience a similar sense of bereavement when markets fall which requires a period of mourning. He therefore rationalised that an investor would not re-enter the market until this period of mourning has finished. From this behavioural pattern, Coppock created a technical system that identifies recovery patterns in share-markets. While the story is unique, the evidence is compelling and the reason why it is contained on this list.

9. The Average Allocation to Equities – The optimism/pessimism allocation metric is a gauge of household behaviour towards the share-market. It specifically tracks the percentage of household wealth being directed towards personal equities, which has had a history of rising and falling depending on sentiment around fear and greed. If the average household is investing less than average in the share-market, this is considered a sign of excessive pessimism and can be expected increase over time. The same applies in reverse, as a high percentage shows over optimism and can be expected to fall. The inflows/outflows this creates over the long-term has had a significant impact on performance.

Final Thoughts

We can see above that each of these metrics have the ability to idenitify mis-pricing opportunities. There are multiple limitations to each metric, and these need to be understood if you wish to use them as part of your investment philosophy. However, there is a real power of tracking metrics such as the above, especially as a combination, which can be best explained below. We urge readers to add these nine metrics to their watch-lists.

Note: If you wish to see the net result and current standings of these metrics using fundamental rigour, we encourage you to request the latest report as a free one-off trial or by subscribing to our ongoing report.

RECOMMENDED BY THE INVESTING TIMES

We have an unprecedented rise in the over 65 age group and our working population is growing at a more modest rate. This article will detail the real problems we face and how you can profit from it.