Donald Trump and economic stability rarely go hand-in-hand. While Trump insists he’ll “make this country rich again”, his path to riches has been subjected to four bankruptcy negotiations and his vagueness as a potential President can be summarised in “I want to be unpredictable.”

Donald Trump and economic stability rarely go hand-in-hand. While Trump insists he’ll “make this country rich again”, his path to riches has been subjected to four bankruptcy negotiations and his vagueness as a potential President can be summarised in “I want to be unpredictable.”

With the expectation for a close race to the White House in November this year (betting odds apparently have it as 1/3 vs 5/2 in favour of Clinton), it seems likely Donald Trump or Hilary Clinton will inherit a ticking bomb that is called the “debt ceiling”.

The debt ceiling is a piece of legislation that is intended to limit the amount the United States Government can borrow. However, well before Donald Trump rose to prominence politically, the USA Government has been amassing more and more debt, to the tune of $19.29 trillion at the latest recording and counting. This equates to a potentially dangerous ‘Debt to GDP ratio’ of 105.4% and a trajectory that means the last extension of the debt ceiling to March 2017 will need to be renegotiated again early next year.

The problem is this. If the vote is close, which it could easily be, and a majority is not created in Congress, either Trump or Clinton will have a very difficult time agreeing on terms to extend the debt ceiling further. If no agreement is made, the United States Government can’t pay its bills which leads to an abrupt default. The seriousness of this event for the USA should not be under-estimated:

“A default would be unprecedented and has the potential to be catastrophic: Credit markets could freeze, the value of the dollar could plummet, U.S. interest rates could skyrocket, the negative spillovers could reverberate around the world, and there might be a financial crisis and recession that could echo the events of 2008 or worse.” — U.S. Treasury report in 2011

It may not be Donald Trump or Hilary Clinton’s fault that the debt grew so substantially, and it is a complex story on why the United States has opted to take on so much debt along with the majority of the world, but whether it is Donald Trump or Hilary Clinton in office, they will hardly have had a chance to warm their seat before having to deal with this mess. Historically, debt ceiling negotiations have required an 11th hour agreement because the two political parties (Trump’s Republicans and Clinton’s Democrats) cannot agree on policy direction and block it in Congress as a re-negotiation tool.

The last occasion this “debt ceiling” was breached, it was Barack Obama’s “Obamacare” in the firing line. This would seem far less controversial than many of Donald Trump’s policies, meaning a greater risk of a stalemate and increased recessionary risks.

While Trump is known for his comments such as “Rich people are rich because they solve difficult problems”, it is another thing altogether managing a Congress that have conflicting views on policy to the extent as this 2016 Presidential Election.

It would seem Donald Trump himself has been an advocate of a stalemate and willingness to let the United States go into shutdown. His remarks prior to the 2013 debt ceiling negotiation went along the lines of “I don’t think [the United States is] going to go into default, but I do think if we allow laws like this to go through, we’re going to be in much bigger trouble long term” — Donald Trump in 2013

It begs the question on who is a more suitable candidate to lead the United States through a very tricky time politically. Forget the lacklustre growth forecast, the ageing population or the unemployment concerns, the real concern between now and the start of next year is how to handle a potential United States default.

Hilary Clinton does not have a perfect record, and it would appear likely the debt train would continue under her wing, but the alternative is Donald Trump who has been subjected to four Chapter 11 negotiations either directly or indirectly before attempting to take the White House (Trump Taj Mahal in 1991, Trump Plaza in 1992, Trump Hotel & Casino Resorts in 2004 and Trump Entertainment in 2009).

Regardless of the outcome, it is unlikely to be comical if the debt ceiling isn’t dealt with prudently and promptly. So with this in mind, which nominee do you think is better suited?

Quotes on the Debt Ceiling and its Risks:

“We’ve never gotten to the point where the United States government has operated without the ability to borrow. It’s very dangerous. It’s reckless, because the reality is, there are no good choices if we run out of borrowing capacity and we run out of cash.” Senator Jack Lew

“There is precedent for a government shutdown. There’s no precedent for default. We’re the most important economy in the world. We’re the reserve currency of the world. … If money doesn’t flow in, then money doesn’t flow out, so we really haven’t seen this before, and I’m not really anxious to be part of the process that witnesses it.” — Lloyd Blankfein, chief executive of Goldman Sachs

“The debt ceiling is such a calamitous possibility that you could go to a recession or even a depression worse than Lehman and AIG in 2008.” — Senator Chuck Schumer

“To tie [the debt ceiling] to something about whether you break the promises of the United States government to people all over the world as well as its own citizens, just makes no sense. So it ought to banned as a weapon, it should be like nuclear bombs, basically too horrible to use.” — Warren Buffett

RECOMMENDED BY THE INVESTING TIMES

We have an unprecedented rise in the over 65 age group and our working population is growing at a more modest rate. This article will detail the real problems we face and how you can profit from it.

What does it take to identify an impending recession? Obviously, this is an extremely complex question. However, there are at least 10 factors that have had a strong historical track-record of identifying recessions, and below we outline ten metrics to add to your watch-list:

What does it take to identify an impending recession? Obviously, this is an extremely complex question. However, there are at least 10 factors that have had a strong historical track-record of identifying recessions, and below we outline ten metrics to add to your watch-list:

The game of “would-you-rather” is a favourite past-time, usually involving an alcoholic beverage and a willingness to be embarrassed. However have you ever played a clean, moral-based version of the game that helps decode what’s most important to you? See how you answer these tricky questions.

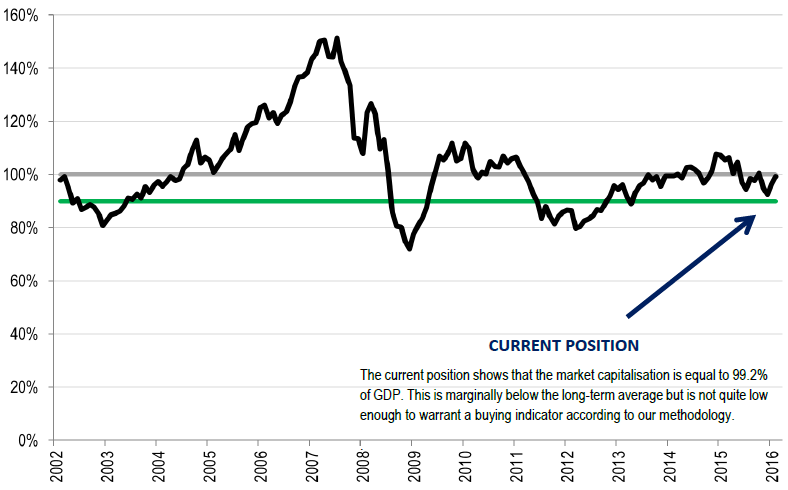

The game of “would-you-rather” is a favourite past-time, usually involving an alcoholic beverage and a willingness to be embarrassed. However have you ever played a clean, moral-based version of the game that helps decode what’s most important to you? See how you answer these tricky questions. Warren Buffett and Robert Shiller should be familiar names to anyone with an active interest in the share-market. They are two of the most respected individuals on the planet when it comes to money matters, and each have varied yet complimentary views on what drives the overall share-market.

Warren Buffett and Robert Shiller should be familiar names to anyone with an active interest in the share-market. They are two of the most respected individuals on the planet when it comes to money matters, and each have varied yet complimentary views on what drives the overall share-market.

China is undoubtedly important to the global economy and with embedded signs of rising bad debts, there are enormous concerns surrounding China’s ongoing stability.

China is undoubtedly important to the global economy and with embedded signs of rising bad debts, there are enormous concerns surrounding China’s ongoing stability. Bad Debt cycles explained

Bad Debt cycles explained